Get our insights delivered directly to your inbox

Sign up to the Finura DigestInvesting In Yourself: Improving Your Financial Wellbeing Is Self-Care

Balancing careers, family responsibilities, and personal aspirations can be overwhelming. Amid this whirlwind, women often rally around each other, offering support for both our physical and mental wellbeing.

However, from personal experience as a financial adviser, and working with others in this industry, it is clear that we must prioritise financial health and welfare alongside our overall wellbeing.

Financial wellbeing can be broken down into two core components; feeling financially secure now and into the future and having the money to help us achieve our personal goals[1], suggesting that financial wellbeing extends beyond mere monetary wealth; it encompasses a sense of security, fulfilment, and freedom.

To achieve financial wellbeing, you must put into place the correct support network and strategies that will help you to work towards financial security. Below, I will highlight some of the key pillars to building financial security.

Pillar 1 – The foundations: emergency funds, budgeting and debt

Addressing these building blocks will allow you to build a strong financial foundation. Emergency funds, of around 3-6 months of expenditure, allow you to cover unexpected costs or support your expenditure in the case of job loss or illness, enabling stability during turbulent times.

Budgeting allows you to track income and expenses to allocate funds wisely, cultivating discipline, and curbing unnecessary spending, which promotes saving, allowing you to feel in control.

Debt management involves understanding and responsibly handling debts, reducing the amount of expensive or unmanageable debt, and promotes debt like mortgages that help you to achieve your life goals.

By nurturing the foundations of your financial plan, you build financial resilience, allowing you to feel more secure now and into the future.

Pillar 2 – Financial Literacy

Women are expected to own 60% of the UK’s wealth by 2025[2], however, with women across the globe having lower financial literacy levels than their male counterparts[3], how can we shift these literacy levels to ensure women can better understand their finances?

Empowering women to engage with their networks and educational resources is key to tackling this financial literacy gap. Engaging in workshops, courses, or with a financial adviser will allow you to discover more about your finances, and plan for specific life events. For example, career breaks for childcare, savings for retirement, and securing your finances following divorce. Education is key for fostering lifelong habits that empower you to manage your finances and grow your wealth.

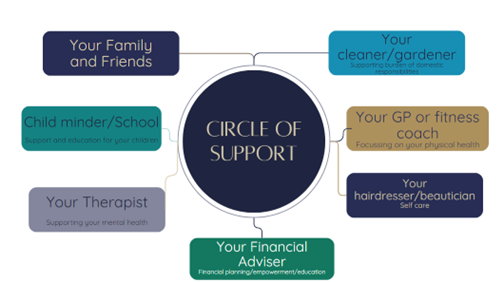

Pillar 3 – Your network and planning for your life goals

Women are fantastic networkers and can maintain a robust Circle of Support, however, with just 36% of women having sought help from a financial planner, compared to 46% of men[4], they often lack the necessary financial adviser connections that can help them receive the education and advice needed to protect and grow their wealth.

Collaborating with a financial planner will enable you to create a personalised road map of your goals and will consider strategies and investments available to help you achieve them, at a risk level that is comfortable for you. This relationship will not only help you to plan but use the correct resources, tools and tax planning to mitigate risk at different life stages, adapt the plans as your life changes and grow your wealth. By leveraging both networks and planning, you can navigate life’s complexities with confidence, realising your ambitions while maintaining financial stability and security.

In conclusion, investing in self-care and personal development is vital for overall wellbeing and financial stability. Key pillars include establishing a strong financial foundation, enhancing financial literacy, and leveraging support networks to plan for life goals. Prioritising physical, mental and financial health builds resilience and confidence in managing finances. Relationships with financial planners empowers you to adapt and navigate life’s complexities. Ultimately, this financial self-care leads to realising aspirations while maintaining financial security.

Written by Lydia Richmond DipPFS, Financial Planner.

Articles on this website are offered only for general information and educational purposes. They are not offered as, and do not constitute, financial advice. You should not act or rely on any information contained in this website without first seeking advice from a professional.

Past performance is not a guide to future performance and may not be repeated. Capital is at risk; investments and the income from them can fall as well as rise and investors may not get back the amounts originally invested.

![]() You are now departing from the regulatory site of Finura. Finura is not responsible for the accuracy of the information contained within the linked site.

You are now departing from the regulatory site of Finura. Finura is not responsible for the accuracy of the information contained within the linked site.

Sources:

[1] Aegon. 2023. “Financial Wellbeing Index 2023.” Aegon.theapsgroup.scot. Aegon. https://aegon.theapsgroup.scot/Financial-wellbeing-2023/8/.

[2] Currie, Maike. 2023. “Is the Future of Wealth Female?” Hargreaves Lansdown. May 26, 2023. https://www.hl.co.uk/news/is-the-future-of-wealth-female.

[3] Bucher-Koenen, Tabea, Annamaria Lusardi, Rob Alessie, and Maarten van Rooij. 2016. “How Financially Literate Are Women? An Overview and New Insights.” Journal of Consumer Affairs 51 (2): 255–83. https://doi.org/10.1111/joca.12121.

[4] Green, Nick. 2023. “Be a Woman with a Financial Plan.” Unbiased.co.uk. September 7, 2023. https://www.unbiased.co.uk/news/financial-adviser/be-a-woman-with-a-financial-plan