Another pension age change

Share

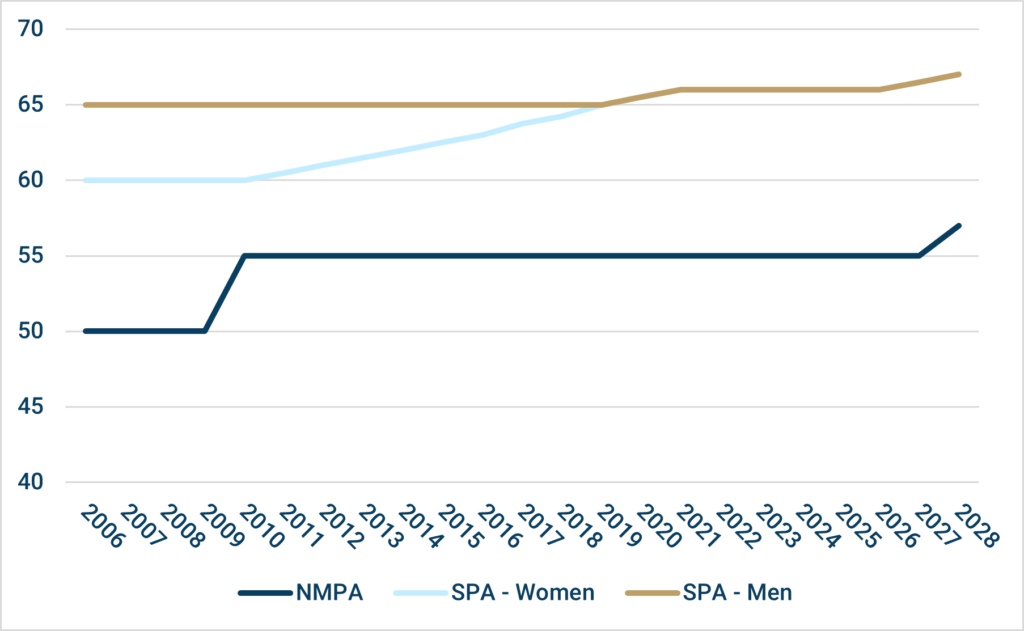

The start of the next increase to state pension age (SPA) is still nearly five years away, at which point it will be phased up to 67 by April 2028. In the meantime, the Government has confirmed a rise in pension age for private pension provision that was originally suggested in March 2014.

The normal minimum pension age

The increase is to be made to the normal minimum pension age (NMPA). This is the earliest age from which non-state pension benefits can be drawn, subject to very limited exceptions. The current NMPA is 55, set in 2010 as 10 years below the then male SPA of 65. The new NMPA from 2028 will be 57, 10 years below what by then will be the SPA for both sexes.

Changing pension ages

The Government has indicated that there will be exceptions to the higher NMPA covering:

- Members of the armed forces, police and fire services pension schemes, who will have a ‘protected pension age’ of 55

- Anyone who has a protected pension age for scheme benefits arising from the last increase in NMPA and

- Anyone who, on 11 February 2021, had a right under a pension scheme to draw benefits before age 57. In this context, the right has to be unqualified, i.e. there must be no requirement for consent from any other person, such as a trustee or employer. It will also apply on an individual scheme basis, so you might find some benefits can be drawn before 57, while others cannot because consent is required

It would appear that if you have a personal pension established by the February cut-off date, you will generally meet the ‘unqualified right’ requirement, giving you a protected pension age of 55. However, some experts believe this could change when the necessary legislation emerges. When the previous NMPA increase was made, there was no such protection for personal pension owners.

Born between April 1971 and April 1973?

If you were born on 6 April 1973, you are potentially the worst hit by the change, unless you have benefits that are subject to a protected pension age. That is because you will reach your 55th birthday on the very day the NMPA increase to 57 takes effect – unlike the changes to SPA, there is no phasing in of the change. If you were born in the preceding two years, you will be in the odd position of being able to draw benefits at age 55 until 5 April 2028, but then need to wait until you reach age 57 before setting up any new drawings from you pension.

A realistic retirement age?

The idea of retiring at 57, yet alone 55 may sound appealing, but is it at all realistic? Consider these two factors for a start:

- At age 57, the average man has 27 years of retirement ahead of him, while the average woman has 30, according to the Office for National Statistics. 1 in 4 of those men will live until age 92, the corresponding age for 25% of women is 94

- From 2028, there will be a gap of at least 10 years before your state pension starts. With the current state pension of £179.60 a week, that means an income hole to fill of at least £93,400 (plus inflationary increases)

A recent report showed that the average age of those ‘retiring’ in 2021 was 60. However, it also revealed:

- 37% had brought forward their retirement in the past year, with the three main reasons being pandemic related

- 27% will work part time to support themselves in retirement

- 37% were worried about not having enough money to last through retirement

- Two thirds of retirees risked running out of money in retirement according to calculations by the report’s authors, even though the planned average total spend was a modest £21,000 a year

The change to a normal minimum pension age of 57 is largely irrelevant – few people can afford to retire so early – but it might affect you if you plan to draw some benefits early, e.g. to clear a mortgage.

Are you sure your planned retirement age is not going to leave you among those two thirds who might run out of money before they pass away? Contact us for an impartial assessment now – the sooner you know where you are, the quicker you can, if necessary, make the necessary adjustments.

The Financial Conduct Authority does not regulate taxation or trust advice. Past performance is not a guide to future performance and may not be repeated. Capital is at risk; investments and the income from them can fall as well as rise.

Articles on this website are offered only for general information and educational purposes. They are not offered as, and do not constitute, financial advice. You should not act or rely on any information contained in this website without first seeking advice from a professional.

Past performance is not a guide to future performance and may not be repeated. Capital is at risk; investments and the income from them can fall as well as rise and investors may not get back the amounts originally invested.

![]() You are now departing from the regulatory site of Finura. Finura is not responsible for the accuracy of the information contained within the linked site.

You are now departing from the regulatory site of Finura. Finura is not responsible for the accuracy of the information contained within the linked site.

Source: Techlink

Share

Other News

Finura in the Spotlight: Shortlisted for Multiple Awards

Finura has an exciting few months ahead, as we wait to see the outcome of a number of short listings in different awards categories. MONEY MARKETING AWARDS – Advice firm of the year The winners will be announced on 12 September 2024 at The Londoner Hotel in London https://moneymarketingawards.co.uk/2024/en/page/shortlist-2024#adviser MONEYAGE AWARDS – Financial Adviser Award: […]

5 Tips For Parents With Children Heading To University

Starting university can be a challenging transition, but with a few lifestyle changes and careful planning, it can be a much smoother and enjoyable experience.

Empowering Yourself For Your Future: The Importance Of Lasting Powers Of Attorney (Property And Financial Affairs)

Life is unpredictable and unforeseen circumstances can sometimes leave us incapable of making decisions about our own affairs. That’s where a Property and Financial Affairs Lasting Power of Attorney (LPA) comes into play.